Veris Residential (NYSE:VRE)

NJ waterfront apartment REIT trading at >25% discount to NAV, 1/5 of portfolio sold or under contract, potential M&A target for listed REITs or REPE

The Jersey City skyline highlighting the additions of VRE’s The Sable and Haus25

Summary

Veris Residential owns a premier portfolio of high-quality, new apartment buildings in high-barrier markets (Jersey City / Port Imperial, Boston, suburban NJ / NY, and DC).

Sold 2 properties and have 2 under binding contract in July at ~5.25% cap rate, have focused on selling smaller deal size, more liquid, but less attractive assets.

At $14.70 per share, Veris Residential trades for a ~6% cap rate and ~27% discount to my estimate of net liquidation value of $20 per share.

NJ waterfront multifamily development sights are conservatively valued by management and could deliver significant upside.

Kushner Real Estate offered $18.50 per share for the company in 2022 in a weaker capital market environment.

Board and CEO, who led liquidation and eventual take private of Northstar Realty Europe, is hand-picked by Madison International Realty and Bow Street, who own ~11% of the company.

President and co-founder of Madison just left board, could be prelude to M&A involvement.

Chief Investment Officer left company in Q2, further indications company will be wound-down.

Background

Veris Residential is a small ($1.5 bn market cap) US multifamily REIT that owns properties in the Northeast, with a large share of its portfolio located on the New Jersey Waterfront (Jersey City & Port Imperial / Weehawken). Formerly known as Mack-Cali Realty Corp, the company rebranded in 2021 to reflect a transition in strategy from owning a diversified mix of property types to focus on multifamily. This transition was largely complete in 2024 with the disposition of their final office properties. Another key event in the company’s history was the redemption of a preferred interest in the residential / multifamily subsidiary held by Rockpoint (a real estate private equity firm) in 2023.

Source: Tikr.com

In late 2022, with the majority of the transition to multifamily complete, Kushner Companies made an unsolicited offer to acquire the company for $16.00 per share. They increased their offer to $18.50 per share, but discussions broke down with each side alleging that the other walked away from the table.

Following the failed take private bid, shares have traded sideways. High leverage, rates remaining elevated, and investor fatigue have weighted on the stock. Furthermore, a bungled proposed equity raise in June of 2024 to fund the acquisition of a property in Port Imperial that was effectively rejected by investors raised questions around the go-forward strategy and management’s alignment with shareholder value.

Why now?

In conjunction with Q4 2024 earnings and 2025 guidance, management outlined an update to their strategic outlook to focus on $300m - $500m of dispositions, comprising the majority of their land bank and select multifamily properties over the next 12 - 24 months, with proceeds used to reduce leverage to below 9.0x net debt / EBITDA and fund up an up to $100m share repurchase program.

They delivered on this plan in a significant way with the announcement of their Q2 2025 results, in which they announced the sale of two multifamily properties for ~$205m with a further two under binding contract for ~$180m. With $60m of land sold to-date in 2025, this would bring total dispositions of $435m in 2025.

The properties sold and under contract are far from the best assets they own. They are located in suburban NJ, NY and in Worcester, MA. They are slightly younger and better occupied than the portfolio on average but have significantly lower average revenue per unit. Management highlighted that they focused on these properties due to their smaller deal size (~$100m per property) where they see more liquidity in the market and were able to achieve prices in line with their view of intrinsic value. These four sales were at a ~5.25% cap rate based on Q2 2025 NOI annualized (5.1% based on trailing twelve month NOI).

While management has outlined a strategy of selling assets to reduce leverage and buy back shares, delevering to a level acceptable to REIT capital markets looks clearly out of reach. Leading multifamily REITs are leveraged between 4x - 6x net debt / EBITDA are Veris’s 9x target does little to close this discount.

What these transaction do achieve is to concentrate shareholders’ interest in Veris’s crown jewels - the Jersey City and Port Imperial properties. I believe this makes the company increasingly attractive to an acquiror, especially a listed REIT peer due to their low cost of debt in the REIT unsecured market.

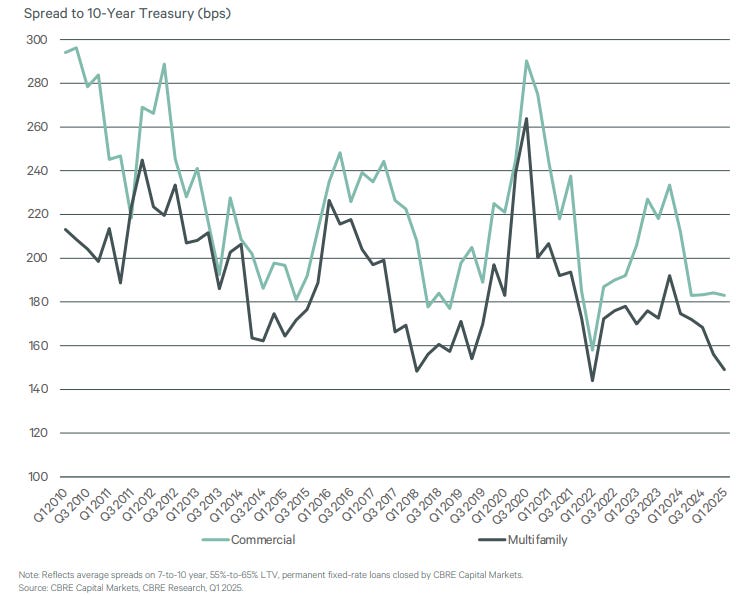

Supporting the sales to-date and a potential larger-scale M&A transaction is the fact that multifamily capital markets have opened back up over the past 12 months with evidence stacking up for high-quality multifamily portfolios trading at a ~5% cap rate and cost of debt falling, expanding the ability of leveraged buyers to re-enter the market.

KKR acquired a $2.1 billion portfolio across coastal and sunbelt markets in June 2024 at a ~5.25% cap rate, Equity Residential acquired a $1 billion portfolio from Blackstone in August 2024, predominantly in sunbelt markets at a 5.0% cap rate, AvalonBay acquired a portfolio of assets in Texas this year for $620m for a sub-5% cap rate and Equity Residential announced the acquisition of a $535m portfolio in Atlanta in May at a high-4% cap rate.

While long-term rates have been largely stable at levels the industry would probably describe as “high” this year, spreads for multifamily financing have continued to come in, reaching a near post-GFC low in Q1 2025 according to CBRE. With the 10 year treasury around 4.5%, this translates into 7yr - 10yr financing rates of ~6%. LTVs available are ~65% after falling to ~60% in 2022. Agency financing can be tighter, in the mid-5%. REIT unsecured financing is tighter still: AvalonBay secured a $450m 4-year term loan in April at a ~4.5% rate and issued $400m of 10-year unsecured notes at 5.08% in June, which reflected just a 85 bp spread to the US 10-year treasury rate.

What’s it worth?

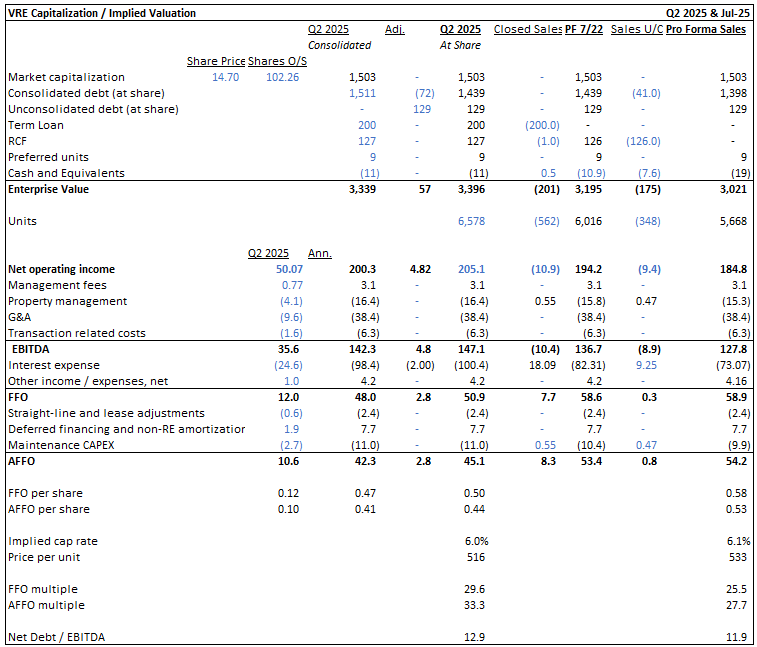

Veris’s financials are a little complex due to non-controlling interests in consolidated JVs and their interest in unconsolidated JVs. In order to assess the price implied by where the stock is trading today, I’ve also made adjustments for the sales closed in July as well as use of proceeds for the properties under contract.

As of Q2 2025, Veris traded at a 6% implied cap rate and ~$520k per unit when accounting for JV interests at share. The dispositions and repayment of debt are accretive - increasing the implied cap rate by ~10 bps to 6.1% and increase my estimates of FFO / AFFO per share by about 15%. They also delever by about 1x turn of EBITDA. The company makes many adjustments to EBITDA, FFO, and AFFO, which I do not so while my estimates track what the company announces, they don’t match 1 to 1. Also to note, while I typically calculate cap rates based on NOI less property management costs, due to moving pieces around management fee and severance I have used reported NOI (and thus, implied and valuation cap rates should be higher than if property management expenses were taken into account).

While these transactions are accretive, make no mistake: Veris is not cheap on a cash flow multiple basis. I see it trading for ~28x AFFO whereas the large coastal multifamily peers trade for ~20x AFFO. Due in part to the sub-scale nature of the portfolio and to a bloated cost structure, property management and G&A expenses are high relative to the REIT’s asset and NOI base.

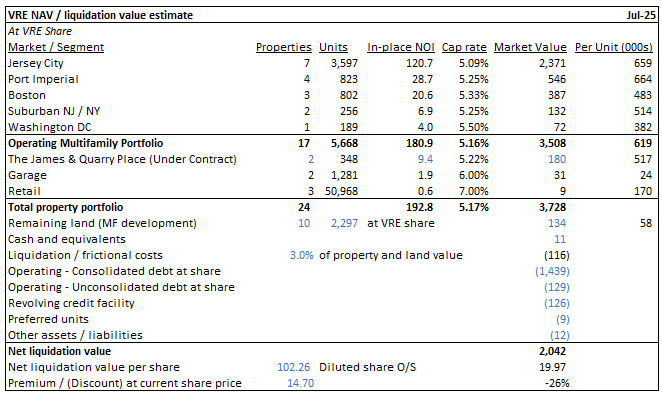

However, I do think that Veris is cheap relative to the private market value of its portfolio. Valuing the Jersey City portfolio at a ~5.1% cap rate and the remaining operating assets between 5.25% - 5.50% results in a valuation of the remaining multifamily portfolio of ~$3.5 billion, a weighted average 5.2% cap rate, and ~$620k per unit.

While the high value per unit figure for the NJ waterfront properties jumps off the page, I think this is actually not far off replacement cost. Veris developed Haus25, located smack-dab in the middle of the Waterfront district of Jersey City in 2022 at a cost of $635k per unit. Furthermore, just this year Boston Properties formed a Joint Venture with Albanese Organization and CrossHarbor Capital to develop a 670-unit scheme at 290 Coles, which is located in a less prime Jersey City location, with an estimated total cost of $600k per unit. 290 Coles is adjacent to Veris’s Soho Lofts, which I value a 5.25% cap rate / $645k per unit. Veris acquired Soho Lofts in 2019 for $700k a unit.

The two properties under contract are valued at their indicated prices, which reflects a 5.22% cap rate / ~$515k per unit, the remaining land is valued at management’s estimate of value, and the retail / garage commercial assets contribute ~$18m of value net of associated debt at Veris’s share. I have assumed that liquidation / frictional costs would be in the order of 3% of real estate assets or ~$115m.

This results in a liquidation value estimate of ~$20.00 per share and today’s share price of $14.70 represents a ~25% discount.

Valuable New Jersey waterfront land represents a potential upside

While I have used management’s estimate of the value of their land, I think their approach is fairly conservative. Their remaining land holdings earmarked for multifamily development represent ~2,300 buildable units at their ownership share (there’s a small parcel in Malden, MA that’s zoned for retail, but let’s ignore that for now). Management estimates that their remaining land is worth $134.2m or just under $60k per buildable unit. However, 1,400 of these units are at two valuable New Jersey Waterfront locations.

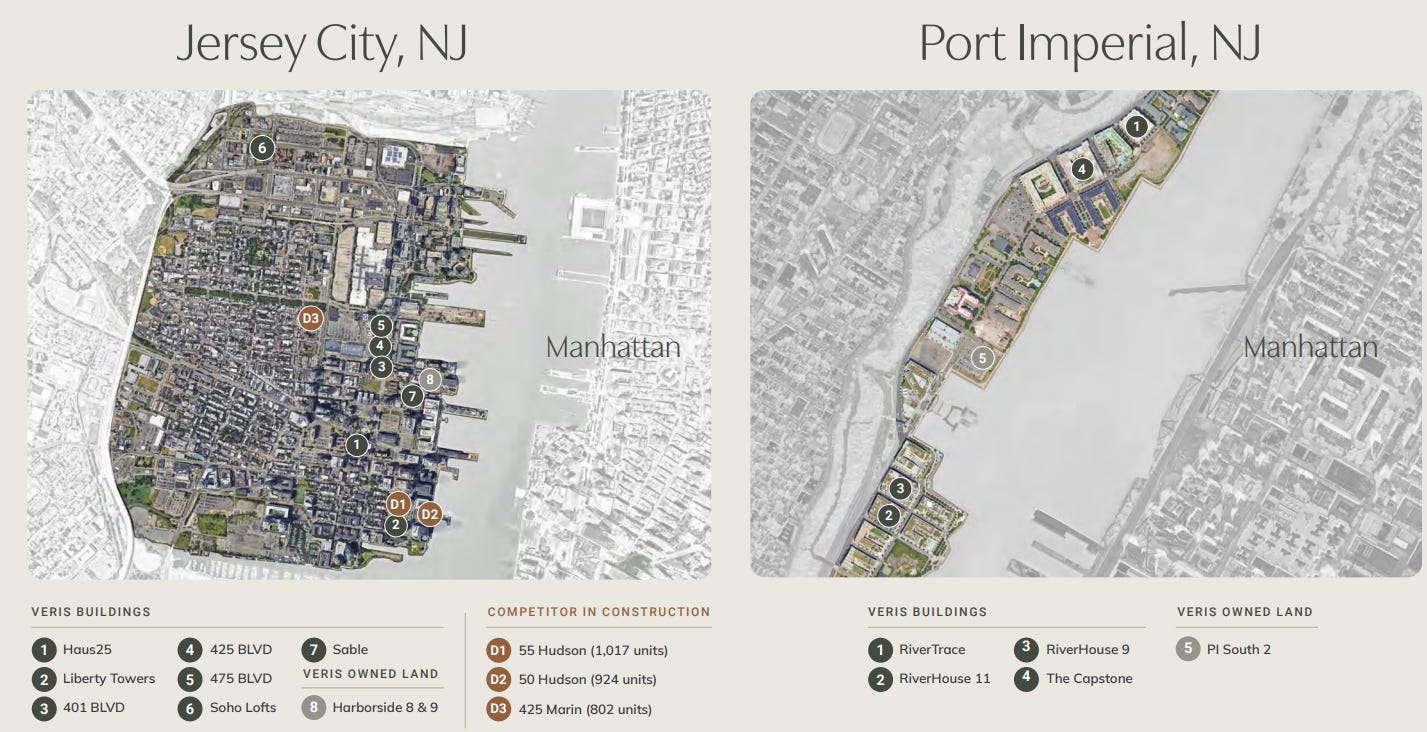

This project consists of two towers - the 68-story Harborside 8 and the 57-story Harborside 9 totaling 1,209 potential units at Veris’s share based on their reporting in the supplemental. The site is 3.9 acres currently used as surface parking. Due to its waterfront location and size, this is an excellent development site.

Veris sold two nearby, but arguably inferior, Jersey City Waterfront development sites in 2023 and 2024 for ~$70k per potential unit and $30m - $45m per acre. One could argue that development conditions have improved since these sales - rates are lower and the trajectory is more clear, rents in Jersey City have grown, and construction costs have likely declined (although tariffs and immigration could reverse this).

Valuing Harborside 8 & 9 at $70k per potential unit would result in a value of $85m or ~$21.7m per acre. As context, a 2-acre site in the Journal Square sub-market of Jersey City, which is a less well-established and appealing, non-waterfront location, sold in March 2025 for ~$24m per acre.

If the site were to be valued at $30m per acre, it would be worth $117m (~$100k per buildable unit) at at $45m per acre it would be worth $175m ($145k per buildable unit). If land value were to represent ~20% of costs (common industry rule of thumb) that would imply total cost of $500k - $725k per unit.

Haus25, which Veris developed in 2022 and “catty-corner” to this site cost ~$635k per unit and generates $43k per unit in annual NOI for a ~6.8% yield on cost. If Harborside 8 & 9 were to generate similar NOI per unit, total cost per unit could be $715k and result in a 6.0% yield on cost and 20% developer margin if valued at a 5.0% cap rate. All hypothetical numbers and hand-wavey to be sure, but this indicates to me that there could be upside to management’s land values from this site alone.

In addition, Veris own a development site in Port Imperial, which represents 191 potential units at their ownership interest (they own ~60% of the site). This was under contract in Q1 for $18.75m at VRE share or ~$100k per potential unit but the deal fell out of bed.

Attractive portfolio for an acquiror

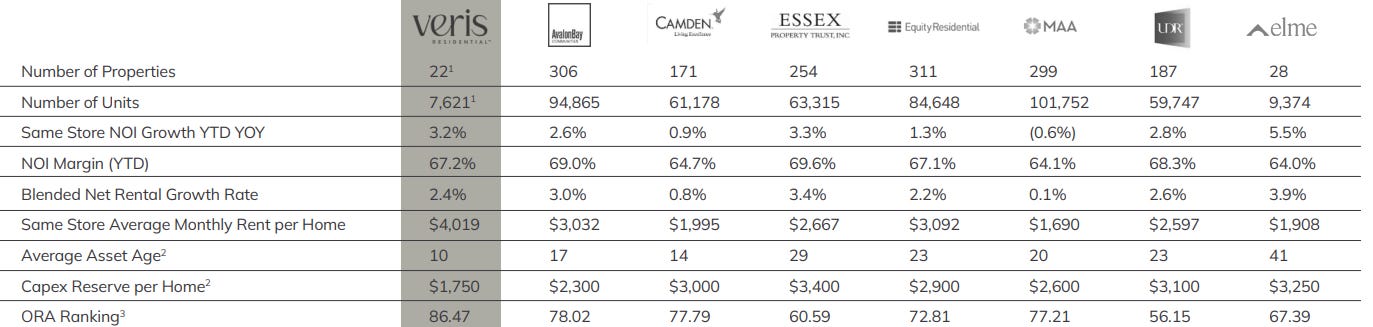

Veris’s portfolio is high-quality and located in strong-performing, high-barrier-to-entry markets. Their portfolio is younger, requires less CAPEX, and generates higher rent per unit compared to their listed peers. They have seen healthy rent growth in their markets, which has translated into strong NOI growth.

Their NJ waterfront properties are highly attractive due to their proximity to Manhattan. This results in an affluent tenant base. Their average rent to income ratio is <11% compared to closer to ~20% for their listed multifamily peers and higher for the wider industry. They mentioned on their Q2 earnings call that 10% of their residents have 7-figure incomes. This is likely to result in less pressure on rents in a downturn and provides headroom for rents to continue to grow without stretching the finances of their tenants.

Multifamily peer benchmarking - Q1 2025 operational metrics

Source: Veris Residential June 2025 Presentation

Incentives and alignment

Board and major shareholders

Two of Veris’s largest shareholders are activist-oriented hedge funds and real estate private equity groups - Madison International Realty, which owns ~6.5% and Bow Street, which owns ~5.5%. Madison built their position in 2019 and Bow Street ran and won a proxy contest in 2020, which replaced 8 out of the 11-member Board and was the catalyst for the REIT’s change in strategy to focus on multifamily, change in the management team, and the (long-suffering) strategic review. Madison’s founder joined the Board in 2023. Effectively, the Board is hand-picked by Madison and Bow Street and I would expect them to act in the interests of shareholders.

Madison will hold their interest in their closed-ended special situations fund series and will want an exit. Rumors at the time of Kushner’s bid were that the Board was looking for a ~5% premium to the improved $18.50 offer price to agree a deal. I feel confident the board would agree to a fair offer to acquire the company.

Management

Mahbod Nia took over as CEO in 2021 after joining the board in 2020. He was previously the CEO of Northstar Realty Europe, which was a spin-off of European assets following the acquisition of Northstar Asset Management by Colony Capital. He successfully executed a “fix-and-flip” liquidation strategy - carrying out value-add intiiatives and selling properties before eventually selling the company to AXA Investment Management. Bow Street were involved in that situation and likely handpicked Mahbod to lead Veris. The remainder of the C-Suite joined subsequent to Mahbod taking over as CEO.

The CEO owns ~0.9% of the company (~800k shares worth ~$11m), and the other members of the C-Suite each own ~0.1% each (~$1.5m). A change in control would result in attractive compensation for the C-Suite that reflect 2x - 3x their annual total compensation.

Reading the tea leaves

In conjunction with Q2 2025 earnings, Ronald Dickerman, the President and Founder of Madison, stepped down from the Board after joining in 2023. One of the reasons cited was “his need to provide Madison with greater flexibility to trade Veris Residential shares in accordance with its fiduciary duty to its fund investors.”

A negative reading of this could be that Madison have given up and intend to sell their shares in order to exit the investment ahead of the end of the fund life it’s held in. A most positive reading would be that leaving the board would give Madison flexibility to work with other investors on a take-private or other M&A transaction.

In addition, the Chief Investment Officer also left the company in Q2, a fact they didn’t announce in the earnings release. This suggests they will not be focused on redeploying sale proceeds into new acquisitions. It will help reduce their bloated G&A structure and increases the probability of M&A in the near-term.

The CEO was pretty negative about both the disposition market and prospects for share repurchases to move the needle going forward. Being uncharitable, maybe there isn’t a plan beyond delever. But he may also be managing expectations around the potential for further asset sales or M&A.

Risks and opportunities

If the company doesn’t get acquired, performance will likely be lackluster due to high G&A and high leverage. Absent M&A, Veris has all the hallmarks of a real estate value trap. It trades at a discount to private market value but with an anemic cash flow yield and virtually no prospects for growth due to high leverage. The good news is that the prospects for a dilutive equity raise are low after that approach was shut down last year.

Elevated near-term (2025-2027) maturities will result in higher interest costs and potentially require cash-in refinancing in some cases. At its share, Veris has $54m of debt maturing in December this year (5.5% interest rate), ~$410m in 2026 (4.2% rate), and ~$240m in 2027 (4.6% rate).

The 2025 maturity reflects VRE’s 40% interest in the Capstone at Port Imperial unconsolidated JV. I think refinancing this loan should be manageable as I see it at ~52% LTV vs. my valuation estimate and a 10% debt yield.

They have 6 2026 maturities, which can be thought of in two buckets: 3 JVs for NJ Waterfront assets and 3 wholly-owned properties, two in Boston and one in suburban New Jersey. The debt maturing at wholly-owned properties totals ~$225m with a ~5.2% rate and management have indicated they plan to refinance using the credit facility (cost of 5.88%). I also think all three of these properties will be near-term disposition targets.

The JV debt totals ~$325m ($200m at VRE share) and will need to be addressed through property-level refinancing. I don’t think any will be near-term disposition targets as they are larger (I estimate property values of $160m, $200m, and $270m for each property). Two of the 3 are well situated with LTVs ~50% and 10%+ debt yields. BLVD 401 has slightly weaker metrics - a 57% LTV and 8.7% debt yield - and will likely be a little more challenging to refinance but doable. With a weighted average rate of 4.0%, interest after refinancing will certainly be higher. If refinanced at say a 5.5% rate, interest expense would increase by ~$4m at VRE’s share, which represents 7% of AFFO. So not terminal but a significant headwind.

Great work, enjoyed reading.

Excellent job. Most incentives seem to be there for a transaction soon but may take a couple years. I wonder if that strange Canadian REIT that just listed would consider a bid to increase their scale.