Dance with the Devil (Nasdaq: ILPT)

Refinancing, lease-up of vacancy, and normalization of dividend creates trade with 20%+ upside

Overview

Source: ILPT May 2026 Investor Presentation

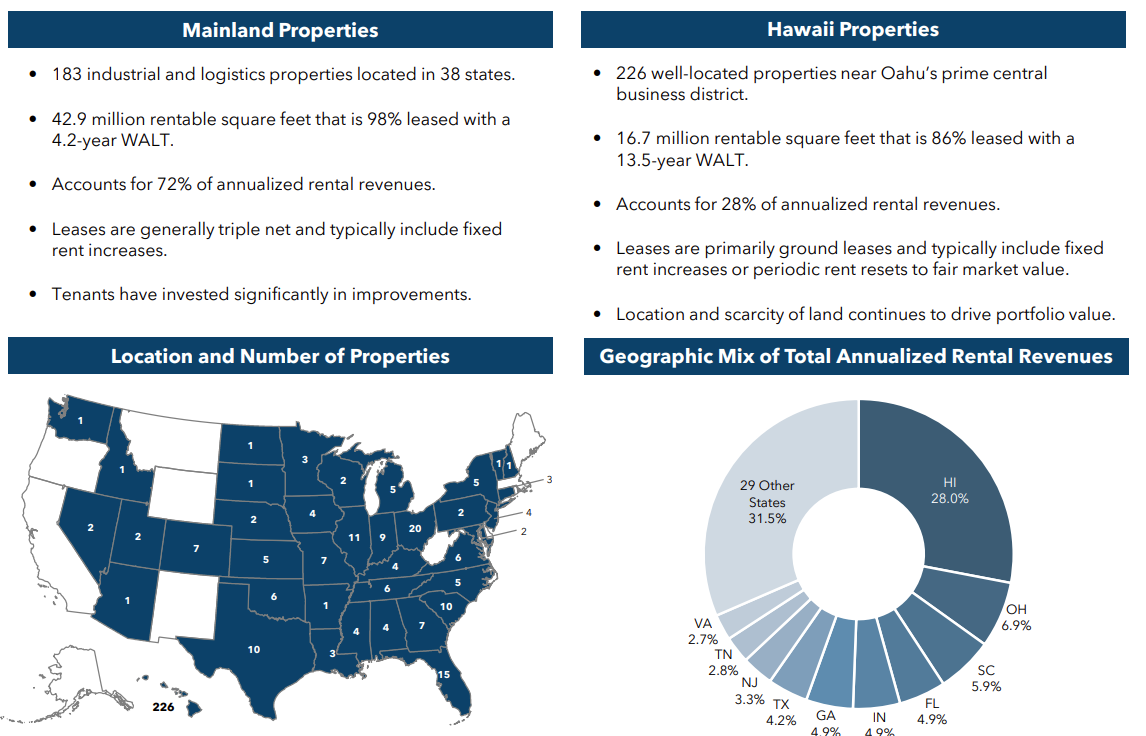

Industrial Logistics Property Trust owns industrial and logistics properties in the US. The portfolio on the mainland is fine - predominantly triple net leased big boxes, 42.9m sq ft, 98% leased, with a 4.2 year WALT.

What makes it interesting are the crown jewels: a 226 property portfolio in Hawaii that represents 28% of annualize rental revenues. A large share of this portfolio is ground leases (common in Hawaii), which provides enhanced credit protection as tenants that don’t renew must hand over the structures they’ve built at their own expense. Barriers to new industrial supply in Hawaii are extremely high due to availability of well-located industrial land, the share of land preserved for conservation, a very high regulatory burden, and high construction costs.

Source: ILPT May 2026 Investor Presentation

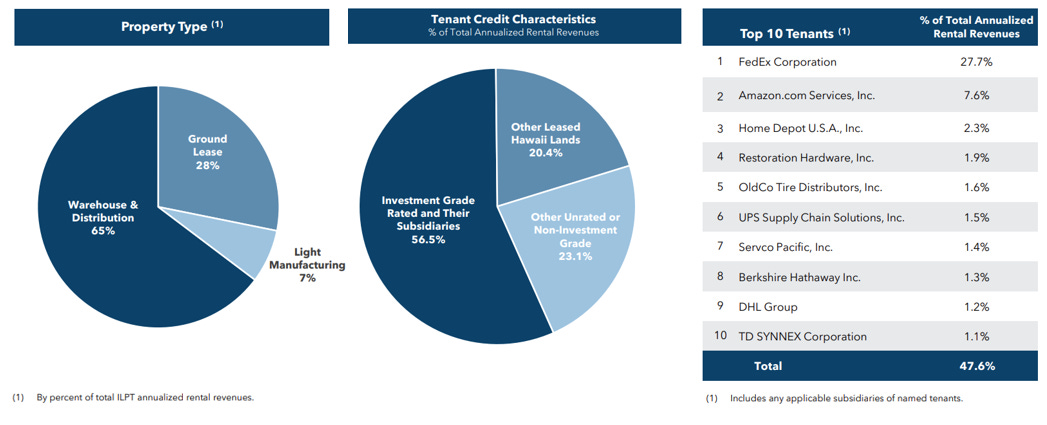

Outside of ground leases - the majority of which are in Hawaii - the portfolio is focused on warehouse and distribution properties with light manufacturing representing just 7% of of revenues. Fedex is the largest tenant by far, mostly by virtue of ILPT’s ill-fated acquisition of Monmouth Real Estate Investment Corporation in 2021 (more on this later).

Source: ILPT May 2026 Investor Presentation

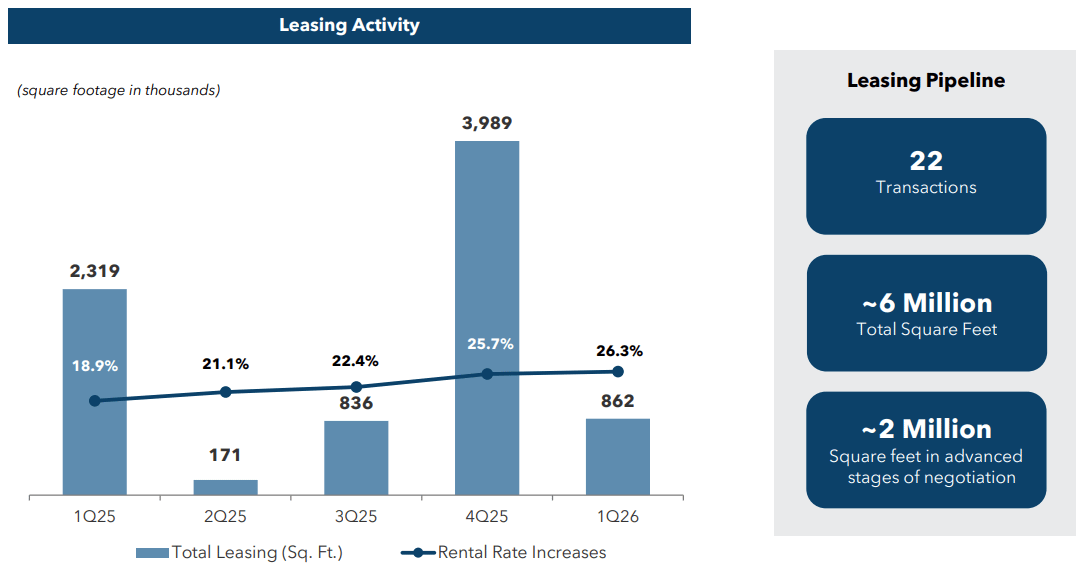

The portfolio has been performing well. Cash basis NOI grew ~4% year on year in Q1 2026, supported by strong occupancy that’s remained above 94% over the past 5 quarters and health spreads on robust leasing activity.

Source: ILPT May 2026 Investor Presentation

Why this opportunity exists

ILPT is externally managed by the RMR group ($RMR). They are one of the best-known, worst-actors in the REIT space. The management contract is for a 20-year term that automatically renews annually. Their management fee is charged on the lower of invested capital and market capitalization, both on a total basis including debt. As a result, they are incentivized primarily to grow the vehicle with the value on a per share basis a secondary concern.

They do earn an incentive fee that is based on outperformance on a per share basis compared to the MSCI U.S. REIT/Industrial REIT index over a 3yr period but after the share price collapsed during the interest rate shock of 2022 (more on this later), this has reset and they’ve started earning incentive fees again in 2025 despite the share price being down ~65% over the past 5 years.

Any RMR-managed vehicle will trade at a discount. One way of expressing this discount is based on the termination fee that would be payable if the management contract was cancelled. For ILPT, I calculate this would be on the order of $300m vs. the equity market capitalization of $600m and enterprise value of $4.2 billion. At my NAV estimate, which I will get into later, this is around a 35% warranted discount to NAV.

Beyond the RMR “stink”, their approach to capital allocation based on their management fee incentives is precisely what got them into the current situation. In late 2021 they agreed to acquire another public US industrial REIT, Monmouth Real Estate Investment Corporation. They were the winner of a bidding war for the REIT and paid peak industrial real estate prices. The acquisition was largely funded by relatively short-term (3yr with 2x 1 year extensions) floating rate debt issued when rates were low.

The lollapalooza effect of an acquisition at peak pricing, using short-term, floating rate debt at trough rates came home to roost almost immediately. Leverage went from <5x net debt to EBITDA and >4x EBITDA interest coverage to >13x net debt / EBITDA and ~1x interest coverage. The CMBS debt structure limited their ability to sell assets to delever and the company had to utilize capital to buy in-the-money interest rate caps to stay on top of interest expenses. In 2023 is was unclear whether the entity would be able survive without issuing highly dilutive equity and they cut the dividend to a nominal quarterly level of $0.01 per share.

Why now?

So why is ILPT interesting today with the share price up ~150% in the past year despite it remaining externally managed by RMR and leverage remaining elevated at 11.6x net debt / EBITDA and 1.4x EBITDA interest coverage?

They have termed out the floating-rate debt that funded the Monmouth acquisition on a 5-year basis, fixed-rate basis, interest-only basis. This has been done in two transactions - a $1.16bn financing in 2025 at 6.4% rate secured by wholly-owned assets and a $1.62bn financing for their Mountain Joint Venture (ILPT own ~67%) at 5.7% rate in May, 2026. This limits maturity risk as they have no consolidated maturities until 2029 (and this is their lowest-leverage pool supported by some of their best assets in Hawaii). They do have $190m of maturities in their unconsolidated jointe venture (ILPT own ~22%) secured by US mainland properties but this JV has a healthy debt yield of ~11% (compared to 7% - 8% for the wholly-owned and Mountain JV portfolios), which supports refinancing. These transactions also mitigate interest rate risk along with the capital needed to purchase rate caps, which has been material over the last couple of years.

As a result, while ILPT’s leverage remains elevated (and will rightfully put off many investors), much of the risk around it has been reduced significantly.

These refinancing transactions improve the predictability of earnings and cash flows, which led to the company reinstating annual FFO guidance in Q1 2026 and ultimately, provides visibility into normalization of the dividend. Management provided normalized FFO guidance of $0.32 per share for Q2 2026 and $1.305 per share for 2026. This is primarily based on ~2.8% year-on-year NOI growth at the midpoint, a deceleration from 4.1% in Q1 2026 and the May 2026 refinancing terms.

ILPT currently pays a dividend of at a rate of $0.20 per year. This represents a <20% payout ratio based on normalized FFO and ~30% of rolling four-quarter cash available for distribution (a metric similar to AFFO). A low payout ratio has allowed them to retain significant amounts of capital, much of which was required to fund interest rate caps and be held in reserve to address refinancing needs. This is no longer necessary.

ILPT has addressed their two largest vacancies within the portfolio ahead of schedule, setting them up to achieve the high-end (or beat) their 2026 guidance range and carry growth into 2027. Just recently (in June 2026) they announced a lease to Fedex for a 10-year lease term for a ~530k sq ft vacant property in Indianapolis, which commenced on May 1, 2026 and had been vacant since August 2024 along with a long-term (53-year) ground lease for 2.2m sq ft in Kapolei, Hawaii commencing on July 1, 2026. Their 2026 guidance had assumed the Indianapolis property would be leased in June (so was achieved 1 month ahead of schedule) and the Hawaii property remained vacant for the balance of the year.

They did not announce financial terms in the press release but we can estimate the impact. CBRE estimates that market rents for Indianapolis warehouse / distribution properties of ~500k sq ft in this submarket are $5.75 - $6.25 PSF on a triple-net basis. If we assume $5.50 PSF, that results in net rent of $2.9m or $0.044 on FFO on an annual basis. At REITWeek 2026 Management indicated that the previous rent at the Kapolei, Hawaii property was equivalent to $0.03 per share of FFO.

Putting this together with the timing of the commencement of each lease, this results in a positive impact to the $1.305 midpoint of normalized FFO guidance of $0.016 per share in 2026 (resulting in $1.321 per share, 1.2% increase) and $0.056 per share in 2027 (resulting in a like-for-like $1.361 per share, a 4.3% increase).

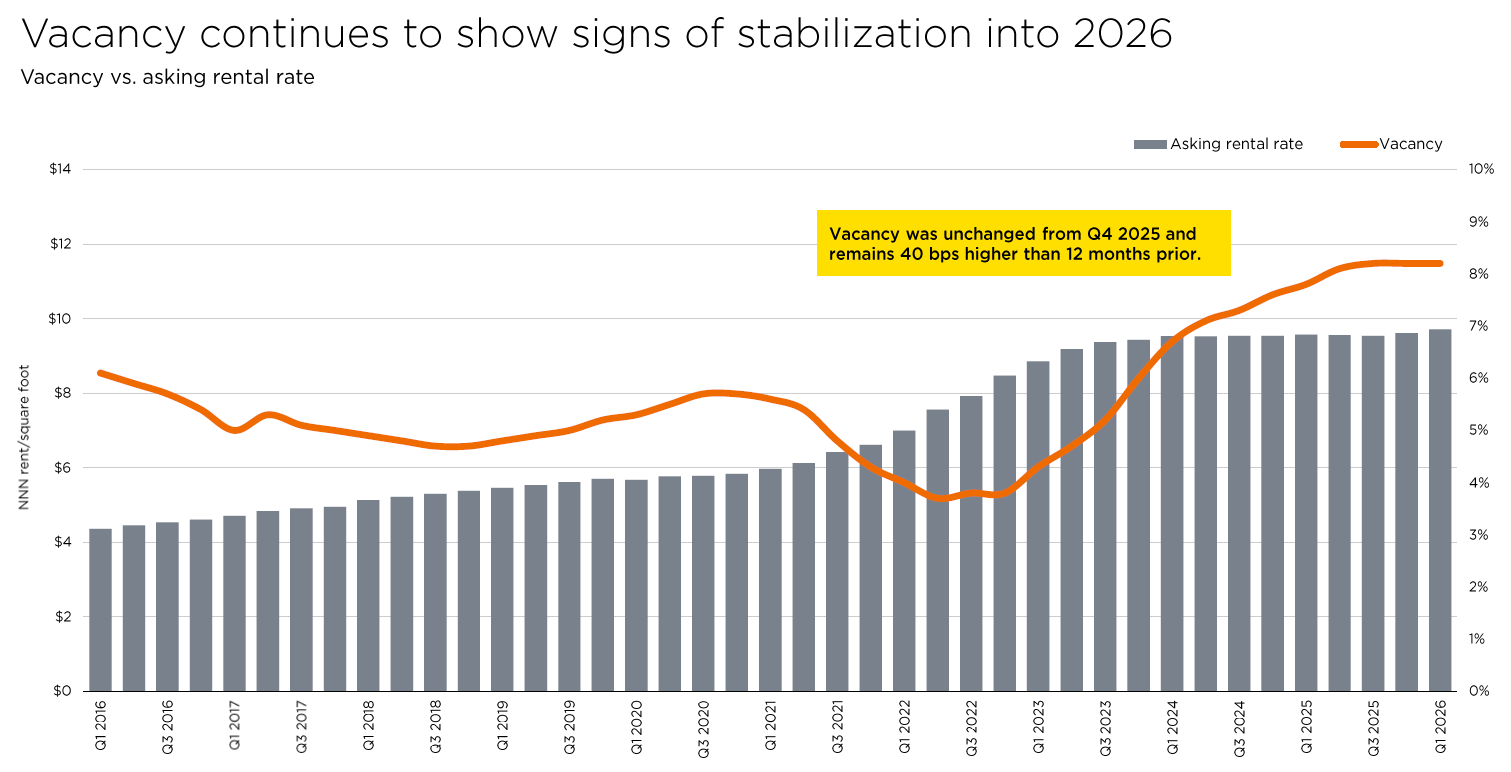

US industrial real estate markets show signs of normalizing and new supply has declined significantly, supporting ILPT’s ability to renew leases and increase rents in coming years. ILPT has a relatively long WALT of 7.4yrs (by rental revenue and has limited lease expiries in 2026 (3.1% of rental revenues) but approximately 10% of leases expire per year 2027 - 2030.

Source: Savills State of the U.S. Industrial Market Q1 2026

US industrial real estate vacancy has risen significantly from its 2022 trough to 8.2% but appears to have stabilized. Rents, which had not growth since 2023, showed ~1% growth in Q1 2026 quarter-on-quarter (and year-on-year).

Source: Savills State of the U.S. Industrial Market Q1 2026

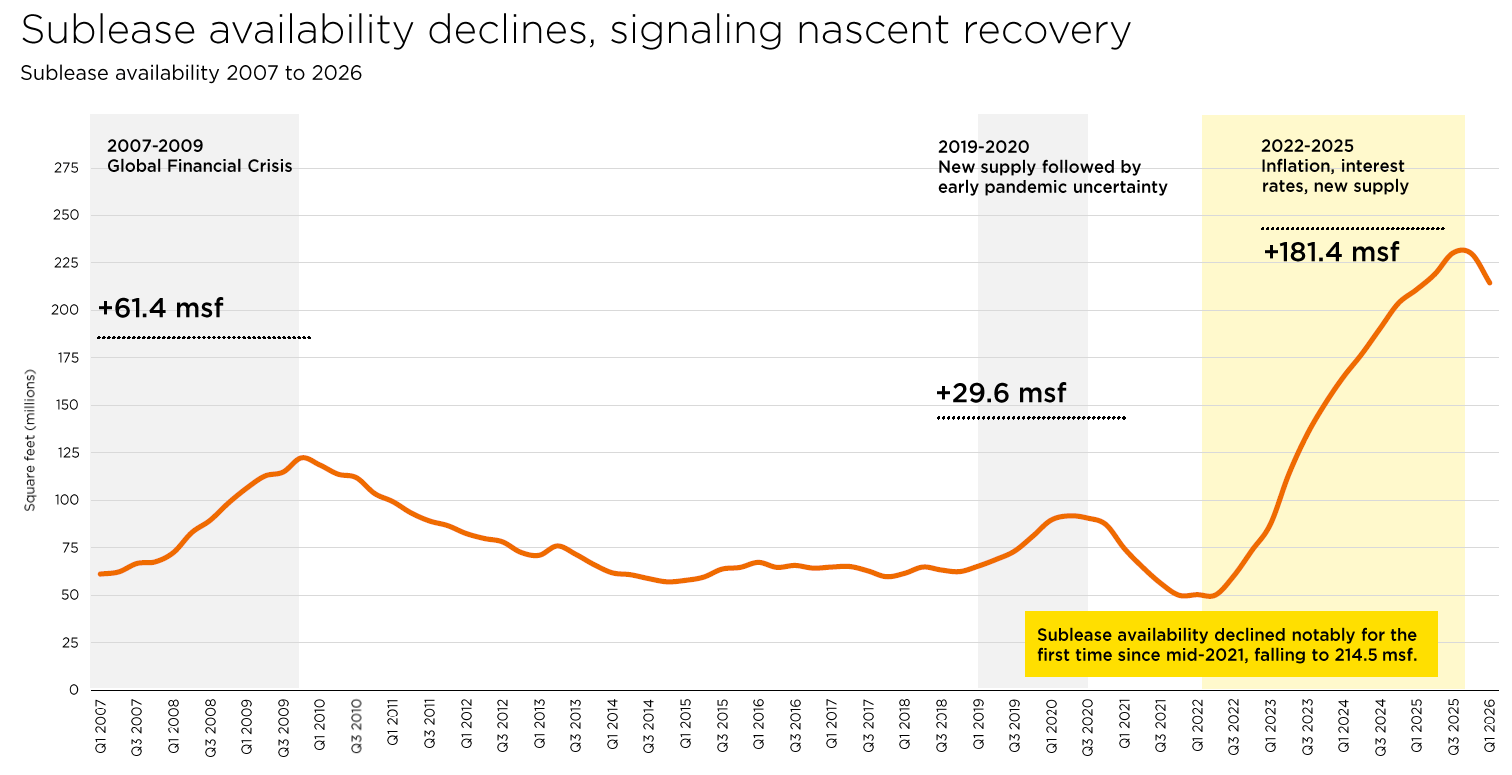

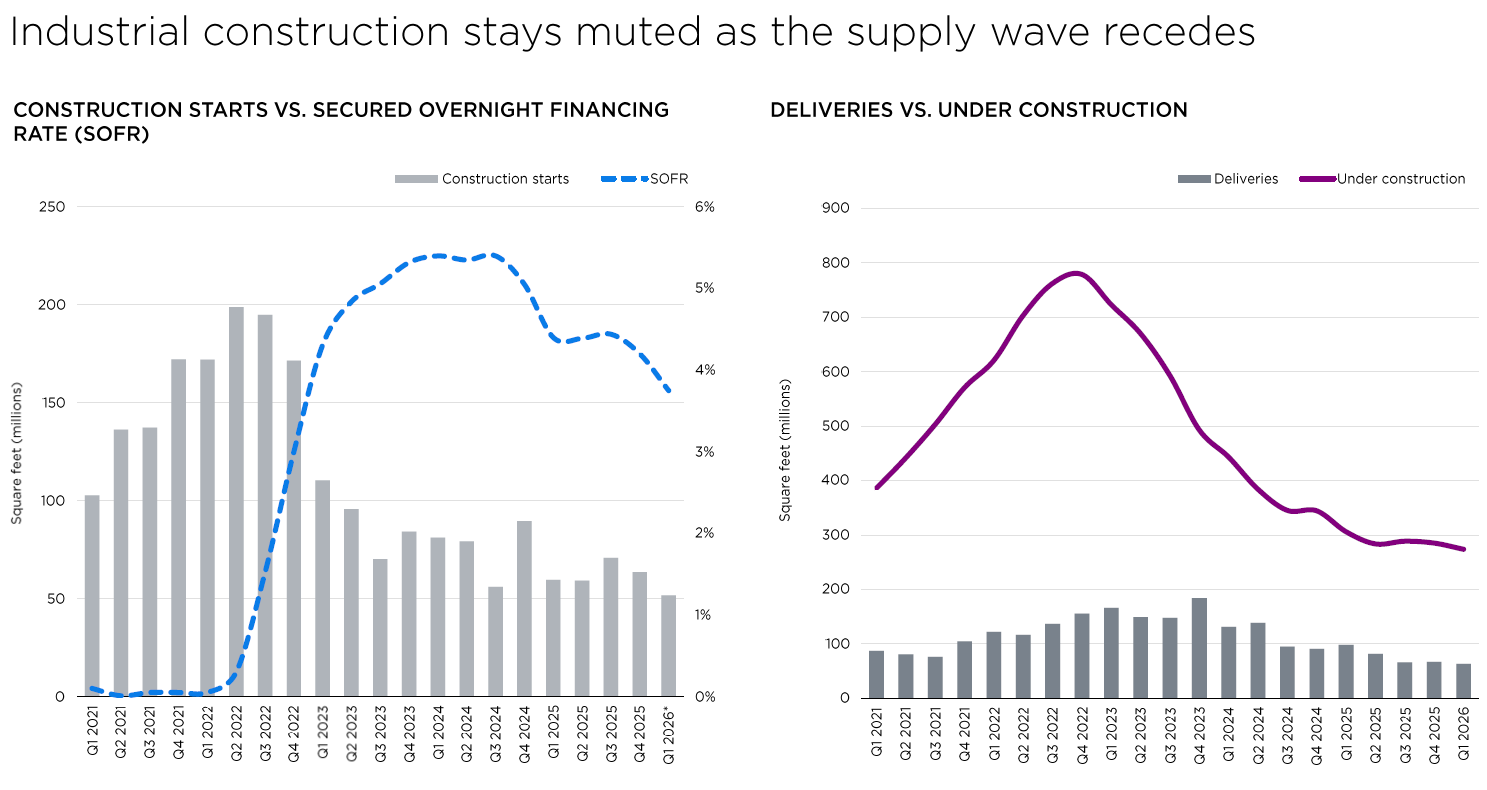

Sub-lease vacancy has turned the quarter, declining notably for the first time in Q1 2026. This indicates that fewer occupiers have excess capacity. Most importantly, new supply has declined signficantly with space under construction below 300m sq ft (from a peak of nearly 800m sq ft in 2022) with new starts running at 200m - 250m sq ft.

Source: Savills State of the U.S. Industrial Market Q1 2026

Plenty of risks remain to US industrial real estate if a recession leads to lower consumer spending, if occupiers are impacted by higher energy prices, etc. but the environment today is significantly more supportive than it has been for the last several years.

What I think it could be worth

At $9.00 per share, ILPT trades at an implied cap rate of 7.4% and $77 PSF. I adjust for the non-controlling interest in the unconsolidated Mountain JV and ILPT’s share of the unconsolidated “The Industrial Fund” JV. This reflects a ~7x multiple of management’s 2026 normalized FFO guidance of $1.305 per share and I see a 10x AFFO multiple assuming CAPEX of ~8% of cash NOI ($25m in total vs. $23m incurred in 2025 and $17m in 2024).

Let’s harbor no illusions - I believe RMR will never let this company be acquired nor undertake shareholder-friendly improvements to its management agreement. The investor base for RMR-managed vehicles has been - in my opinion - yield-focused investors.

As a result, as much as it pains me to do so as a through and through “NAV boi”, I think the most appropriate way to value ILPT is on a dividend yield basis. I believe that now that they’ve resolved their major upcoming debt maturities and leased their largest vacancies, ILPT will increase their dividend back towards normalized levels over the next 12 - 18 months. Even if they wanted to continue to retain capital to deleverage, acquire new properties, etc. they will be limited in their capacity to do so by REIT requirements to pay out 90%+ of taxable income.

Leaving aside the highest-quality industrial REITs (such as Prologis, First Industrial, East Group, Terreno Realty, etc.) and focusing in on those that focus more on net lease, large assets with portfolio and or governance problems - external management, portfolio that include worse property types, like office, etc. it feels like a reasonable dividend range would be 7% - 8%:

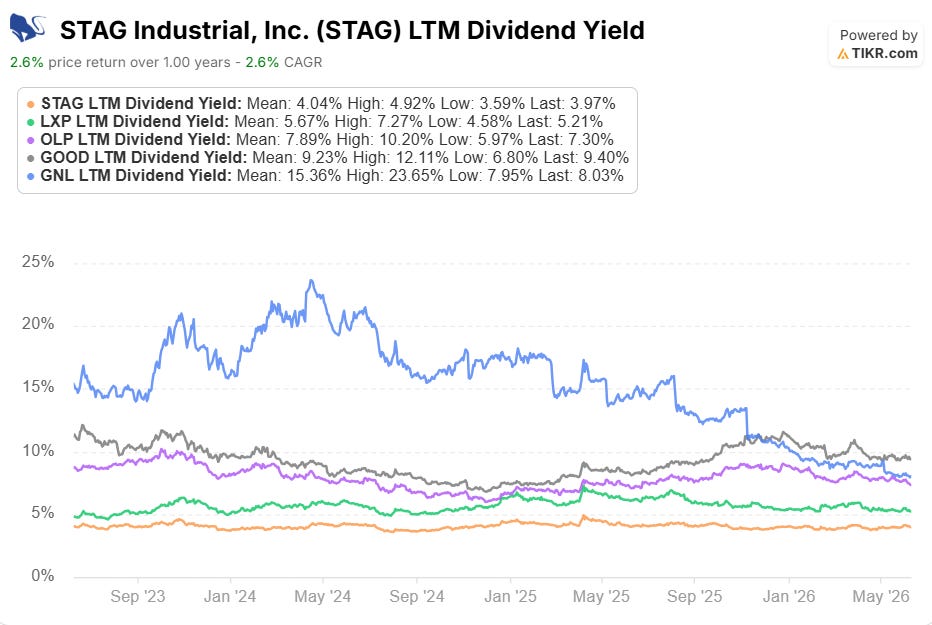

Internally-managed REITs with portfolios that are larger bulk distribution and net leases - LXP 0.00%↑ and STAG 0.00%↑ - trade at 4% - 5% dividend yields

Internally-managed REITs with major governance questions and mixed portfolios that focus on industrial but include office (along with mediocre retail and other) - GNL 0.00%↑ and OLP 0.00%↑ - trade at 7% - 8% dividend yields.

The worst case - GOOD 0.00%↑ - is externally-managed and ~30% of the portfolio is office and trades at a 9.4% dividend yield (and has traded at much higher yields in the past).

I think a 7% - 8% dividend yield gives ILPT basically no credit for the quality of its portfolio, especially the Hawaii assets, or for the built-in FFO growth I see for 2027 based on announced lease transactions, let alone any continued NOI growth through run of the mill leasing.

Before cutting the dividend due its financing issues following the Monmouth acquisition, ILPT paid out ~70% of normalized FFO as a dividend. While they do not disclose taxable income, REITs in general are rarely able to sustain FFO payout ratios lower than 60% due to the requirement to pay out 90%+ of taxable income.

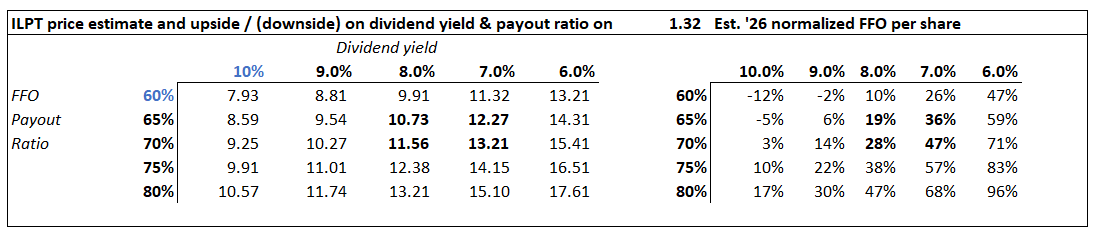

Based on my estimate of 2026 normalized FFO of $1.32 per share (management’s guidance midpoint plus the effect of announced lease transactions), I expect they will increase the dividend towards ~$0.92 over the next year or so. This is approximately 100% of AFFO. If ILPT trades at a 7.5% dividend yield, this implies the stock is worth ~$12.30 - ~35% upside to today’s share price. A range of dividend payout ratios and yields indicate that a really negative case (10% dividend yield, 60% payout ratio) would result in 12% downside to the current share price. If ILPT earns a dividend yield anywhere close to higher-quality peers, there could be a lot more upside.

I don’t think ILPT will increase the dividend all at once. I expect it to happen over 2-3 dividend increases through the remainder of 2026 and 2027. If ILPT increases their dividend to $0.86 - $0.92 per share (65% - 70% normalized FFO) over 18 months, this would result in a 12% - 29% annualized share price return. Dividends received during this period would add to this return and depend on the trajectory of dividend hikes.

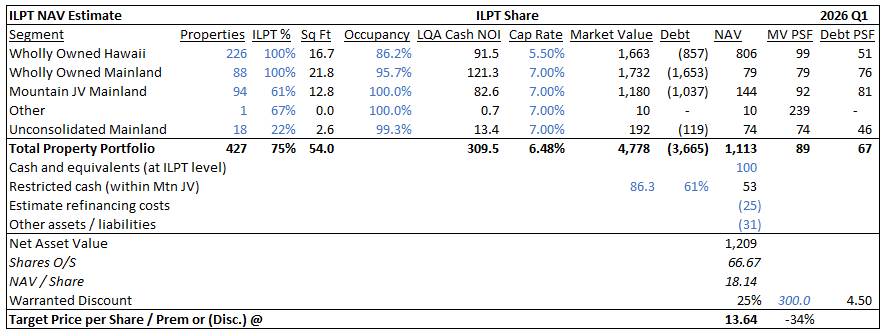

We can use a NAV-based valuation as a sense check on these estimates. Valuing the Hawaii portfolio at a 5.5% cap rate and the mainland portfolio at a 7.0% cap rate, I estimate the portfolio is worth $4.8bn, a weighted average 6.5% cap rate, and ~$90 PSF. This results in a NAV per share of ~$18 before accounting for the onerous RMR management contract. I estimate the termination fee for this would be ~$300m or $4.50 per share, bringing the “warranted NAV” down to ~$13.60 per share.

The calculation of the termination fee is a little complicated but its effectively the present value of the management fee over the 20 years of the management contract discounted at the US 10yr treasury rate + 3.00%. Which is crazy, but a contract.

Risks

RMR does something to benefit themselves at the detriment to shareholders. Over a long-enough horizon the probability of this happening increases to 1, which is why I view this as a trade rather than a long-term investment. In the near-term I think there are limited levers they can pull to really screw shareholders. The biggest risk is that the issue equity with the share price up significantly over the past year. This would be very dilutive to NAV and moderately dilutive - but probably not all that much - to FFO per share. I think some of the risk is reduced by the fact that the normalization of the dividend hasn’t happened yet and my bet is that as the dividend yield increases and shows year on year growth it will hit the screens of retail “pigs”.

Interest rates increase significantly at both short and long-end due to persistent, elevated inflation. This would likely drive higher cap rates and erode the value of their long-leased real estate portfolio. The probability of this is probably reasonably high but direct impacts of this are now lessened by floating rate debt termed out and transitioned to fixed rate. Furthermore, a limited amount of debt matures over the next 3 years (just ~$40m at ILPT share in the unconsolidated JV). But elevated and uncertain rates could impact the yield investors want from an investment in IPLT resulting in a lower share price.

Recession impacts demand in the US industrial occupier market. ILPT’s overall WALT is 7.4yrs but a lot of that is due to long-dated Hawaii ground leases. The mainland portfolio has a 4.2yr WALT and overall, ~10% of leases by rent expire each year between 2027 and 2030. A longer WALT and a manageable number of leases expiring each year insulates ILPT somewhat from a recession and reduced demand for space. In addition, the fact they’ve achieved rent uplifts of ~25% on renewals and new leasing in recent years indicates that their in-place rents are broadly below market, providing some incremental downside protection. Lastly, ~55% of their tenancy is investment grade, which provides some level of mitigation against tenant failure in a downturn across over half of their portfolio. All that being said, industrial real estate is economically sensitive and a downturn would be expected to result in lower retention rates, higher vacancy, and lower rents for the market and ILPT’s portfolio.

Inspiration for the post title: “Dance with the Devil” by Immortal Technique. listener beware, extremely NSFW and probably NSFL, but blew my (teenage) mind when I first heard it.

Really interesting article! Will be following what mngmt does during the next qrtrs .

Thanks for sharing

Nice write up. The Hawaii industrial portfolio is very compelling. But I think I have to take a pass on ILPT. Your assessment of RMR makes this a no-go: "They are one of the best-known, worst-actors in the REIT space..." I think management must be aligned with shareholders.